NTN Connectivity May 2026

The April 2026 report highlights the accelerating presence of non-terrestrial networks (NTN) and satellite connectivity. There is growing interest in satellite communication, with 275 publicly announced operator–satellite partnerships in 101 countries and territories as of April 2026.

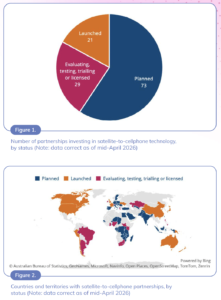

Satellite-to-cellphone services are grabbing the headlines, and several recent transactions promise to change the dynamics of the industry. So far, 21 partnerships have launched services. Initial progress was led by Asia and North America, but this report outlines growing interest in Europe, with the first service launched in Western Europe in February 2026. A further 29 partnerships are trialling the technology and 73 are in planning stage, indicating that there will be further launches in 2026 and beyond.

Community and enterprise broadband accounts for 38% of all partnerships announced between satellite network operators and telecom operators, partly thanks to the technology being more widely available for longer. In contrast, satellite IoT and M2M is beginning to gain traction, although it is stifled by long replacement cycles. Satellite backhaul reported growth in the quarter, mainly owing to a major announcement spanning Europe and Africa.

The United States has the most satellite vendors, including companies such as SpaceX Starlink and AST SpaceMobile. China has the second-highest number of constellations, with seven. A growing number of countries have a satellite constellation either planned or launched, as recorded in GSA’s database, including Taiwan, France and Canada.

A limited number of devices have satellite compatibility using 3GPP narrowband NTN standards. Other devices have been modified to work with certain constellations. Furthermore, some satellite-to-cellphone constellations rely on IMT spectrum which, theoretically, would work with any 4G or 5G smartphone.

Summary:

Satellite technology is rapidly gaining prominence in the cellular and fixed broadband segments. In the past few years, satellite broadband offerings have increased dramatically, driven by deployment of new low-Earth-orbit (LEO) constellations. In addition, satellite connectivity on standard smartphones, referred to as satellite-to-cellphone services, has launched in several markets and continues to gain traction.

Mobile plans including satellite services tend to cost more than those offering terrestrial telecommunication services because of higher hardware costs and the lower capacity of satellite networks. However, satellite launch costs are falling, making it cheaper to add network capacity. The development of 3GPP standards, such as the non-terrestrial network (NTN) capabilities included in Release 17, play an important role in enabling direct-to-cellphone services by greatly increasing the number of compatible devices. Over the next decade, satellite networks are expected to become more prominent.

This report examines the progress of satellite connectivity and how the landscape is set to develop in 2026 and beyond. It draws on public information collected by GSA, focusing on:

- Announced partnerships between mobile network operators and satellite providers

- Uses for satellite connectivity

- Status of commercial services

- Geographic availability

- Frequency bands being earmarked for NTN use

- Examples of chipsets and devices compatible with non-terrestrial connectivity.

As the technology advances and more partnerships are formed, the potential for satellite networks to supplement and enhance terrestrial networks will become increasingly clear.

By mid-April 2026, GSA had identified 275 publicly announced partnerships between operators and satellite vendors for various uses. This marks an increase of 18% since the previous version of this report in February 2026. These partnerships span 101 countries and territories. In total, 180 operators in 84 countries and territories have planned satellite services, and 38 operators in 23 markets are currently evaluating, testing or trialling, or hold licences for such services. Notably, 57 operators in 35 countries and territories have launched commercial offerings, an increase of 10 operators and one country or territory since the previous update in February 2026.

Satellite-to-cellphone

Satellite-to-cellphone is a hot topic in the mobile devices industry because it can theoretically connect any user in remote and rural areas.

Companies offering this capability use terrestrial frequency spectrum owned by mobile operators rather than dedicated satellite frequencies. Active companies include SpaceX Starlink, AST SpaceMobile and Lynk.

However, there has been a movement toward use of MSS spectrum, which enables additional, dedicated bandwidth for satellite communications. This helps mitigate issues with spectrum interference and deliver services more broadly and more powerfully.

For example, SpaceX has purchased licences for MSS spectrum from EchoStar, and Lynk’s proposed merger with Omnispace plans to use some of the latter’s MSS spectrum for a satellite-to-cellphone service. GSA also notes AST SpaceMobile’s purchase of Ligado and Amazon’s planned acquisition of Globalstar, both of which hold MSS licences. As of mid-April 2026, 21 partnerships have launched satellite-to-cellphone services. In March 2026, Kyivstar in Ukraine announced the launch of its service with SpaceX Starlink, which now has more than 5 million connections and has transmitted over 7 million SMS messages. Notable recent launches include Spark in New Zealand and SoftBank in Japan. Both operators have partnered with SpaceX Starlink.

There are currently 29 partnerships that are evaluating, testing or trialling the technology, or hold licences to do so. A further 73 plan to launch (see Figure 1).

Satellite-to-cellphone services have been launched in 17 countries, up from 15 in the previous edition of this report. Several European operators have partnered with the AST SpaceMobile–Vodafone joint venture, branded Satellite Connect Europe, to provide satellite-to-cellphone services. A notable partner is CK Hutchison, which has subsidiaries in Denmark, Ireland, Austria and Sweden. Additionally, Deutsche Telekom has partnered with Starlink to provide services in its 10 European markets, including countries like Austria, Germany and Greece. Notably, several operators are pursuing multivendor strategies for satellite-to-cellphone services. Virgin Media O2, a subsidiary of Liberty Global and Telefonica, was the first operator in the United Kingdom to launch a satellite service. However, Telefonica has partnered with Satellite Connect Europe to explore opportunities in Germany and Spain.

Operators in 61 countries and territories are planning, evaluating, testing, licensed for, or have launched satellite-to-cellphone partnerships (see Figure 2). Of these, Argentina, Brazil, Ghana, Greece, Guam, Ireland, Kazakhstan, Nigeria, Northern Mariana Islands, the Philippines, South Africa, South Sudan and Switzerland are evaluating, testing or trialling, or have licences. A further 47 countries are planning services.

Satellite Providers

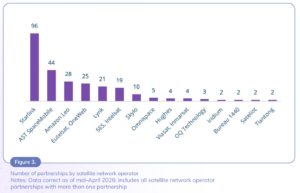

Figure 3 shows the number of publicly announced partnerships by provider. As of April 2026, Starlink has extended its lead with 96 partnerships, up significantly from 59 in January 2026. It is followed by AST SpaceMobile, with 44 partnerships. Amazon Leo, Eutelsat and Lynk round out the top five with 28, 25 and 21 partnerships, respectively.

© GSA 2026

WeChat: GSA Express

NTN Connectivity May 2026